Are you a real estate investor looking to expand your portfolio without relying on personal income verification? The DSCR Investor Cash Flow Loan might be the solution you’ve been searching for. This type of mortgage, also known as a Debt Service Coverage Ratio loan, focuses on the property’s rental income potential rather than your W-2s, tax returns, or employment history. It’s designed specifically for purchasing or refinancing investment properties like short-term rentals, long-term rentals, and even condotels.

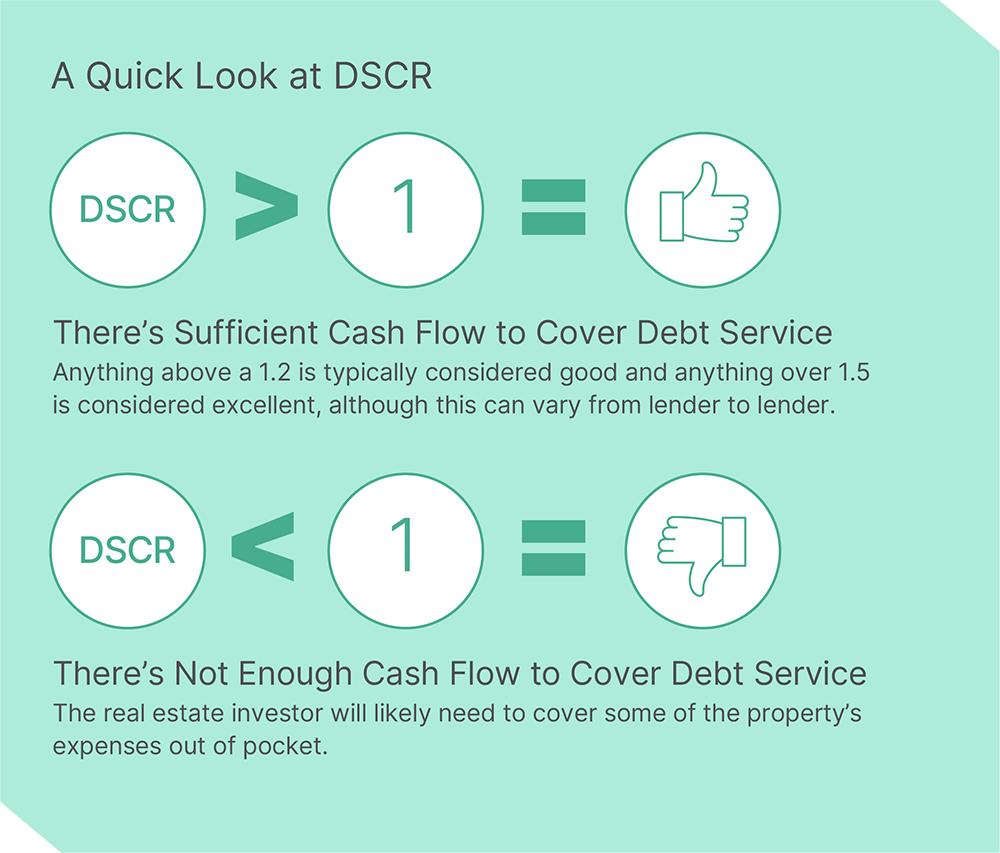

A quick look at DSCR ratios and their implications for cash flow.

Inspired by popular investor tools, this loan allows for financing up to $3 million, with options for purchase, cash-out, or rate-term refinance. Properties can be held in an LLC’s name, and there’s no limit on the total number of properties you can finance. Best of all, qualification is based on a simple analysis of the property’s rental cash flow. However, conditions apply—contact us to see if you qualify.

In this comprehensive guide, we’ll cover everything you need to know about DSCR loans, including general qualifications, benefits, frequently asked questions, and how to get started.

What Is a DSCR Investor Cash Flow Loan?

A DSCR loan is a non-qualified mortgage (non-QM) product tailored for real estate investors. Unlike traditional mortgages that scrutinize your personal finances, DSCR loans evaluate the property’s ability to generate enough rental income to cover its debt obligations. The key metric here is the Debt Service Coverage Ratio (DSCR), calculated as:

DSCR = Net Operating Income (NOI) / Total Debt Service

- Net Operating Income (NOI): This is the property’s annual rental income minus operating expenses (like taxes, insurance, and HOA fees, but typically not property management fees for residential DSCR loans).

- Total Debt Service: Includes principal, interest, taxes, insurance, and any HOA dues (often abbreviated as PITIA).

If the DSCR is 1.0 or higher, the property’s cash flow is considered sufficient to service the loan. Many lenders prefer a ratio of 1.25 or above for added security. This approach makes DSCR loans ideal for investors who may have irregular income, multiple properties, or prefer to keep their personal finances private.

These loans are commonly used for 1-4 unit residential properties that are non-owner-occupied. They offer flexibility for both novice and experienced investors, allowing you to scale your portfolio without the hurdles of conventional financing.

Overview of Investor Cash Flow Loan Program features.

General Qualifications for a DSCR Loan

Qualifying for a DSCR Investor Cash Flow Loan is straightforward compared to traditional mortgages, but lenders still have standards to ensure the investment is viable. Here’s a breakdown of typical requirements:

- Credit Score: Minimum of 620-680, depending on the lender. Higher scores can unlock better rates and higher loan-to-value (LTV) ratios.

- Down Payment or LTV Ratio: Usually 20-25% down for purchases, with LTV up to 80%. For cash-out refinances, it might be lower (e.g., 75%).

- DSCR Ratio: At least 1.0, but often 1.25 for optimal terms. Some lenders allow ratios as low as 0.75 with compensating factors like higher down payments.

- Property Types: Single-family homes, duplexes, triplexes, quadplexes, short-term rentals (e.g., Airbnb), long-term rentals, and condotels. Properties must be in good condition and rent-ready.

- Loan Amount: Up to $3 million per property.

- Reserves: 3-6 months of PITIA in liquid assets, though some lenders waive this for strong DSCR ratios.

- Borrower Requirements: You must own a primary residence. No personal income or employment verification is needed, but a clean credit history helps.

- Entity Ownership: Properties can (and often should) be titled in an LLC for asset protection.

- No Limit on Properties: Unlike Fannie Mae/Freddie Mac loans, which cap at 10 financed properties, DSCR loans have no such restriction.

Keep in mind that these are general guidelines—actual terms vary by lender. Conditions apply, so it’s essential to consult a professional to determine your eligibility.

Benefits and Drawbacks of DSCR Loans

DSCR loans offer significant advantages for investors, but they’re not without trade-offs. Here’s a balanced view:

Pros

- No Income Documentation: Skip W-2s, tax returns, and pay stubs—qualification is property-based.

- Flexibility for Investors: Ideal for self-employed individuals, retirees, or those with complex tax situations.

- Scalability: Finance unlimited properties and close quickly with minimal paperwork.

- Interest-Only Options: Available for 30-year terms, improving cash flow.

- Cash-Out Refinance: Access equity for more investments without personal income checks.

Cons

- Higher Interest Rates: Typically 1-2% above conventional mortgages due to the non-QM nature.

- Larger Down Payments: 20-30% required, which can tie up capital.

- Property Must Cash Flow: If the DSCR is below the threshold, you won’t qualify.

- Limited to Investment Properties: Not for primary residences or fix-and-flips needing major rehab.

Overall, if your property generates strong rental income, the pros often outweigh the cons for serious investors.

Comparison of DSCR loans vs. conventional mortgages.

FAQ: Common Questions About DSCR Investor Cash Flow Loans

Based on top search queries and “People Also Ask” results from Google, here are answers to the most frequently asked questions about DSCR loans.

What is a DSCR loan?

A DSCR loan is a mortgage for investment properties where approval depends on the property’s rental income covering the loan payments, not your personal income.

How do I calculate the DSCR ratio?

Divide the property’s annual net operating income by the annual debt service (PITIA). For example, if NOI is $50,000 and debt service is $40,000, the DSCR is 1.25.

What is the minimum credit score for a DSCR loan?

Most lenders require at least 620, but 680+ is ideal for better terms.

Do DSCR loans require a down payment?

Yes, typically 20-25% for purchases. Higher down payments can compensate for lower DSCR ratios.

Can I get a DSCR loan without income verification?

Absolutely—lenders don’t require W-2s, tax returns, or employment info.

What are the interest rates for DSCR loans?

Rates are usually higher than conventional loans, ranging from 5.5% to 10.5% based on credit, LTV, and property type.

Is a DSCR loan right for beginners?

It can be, but it’s best for those with some experience, as the property needs to demonstrate strong cash flow potential.

Can I use a DSCR loan for short-term rentals?

Yes, many lenders accept Airbnb or VRBO projections for qualification.

For personalized answers, conditions apply—contact us to see if you qualify.

Ready to Unlock Your Next Investment?

Don’t let traditional lending barriers hold back your real estate goals. With a DSCR Investor Cash Flow Loan, you can focus on building wealth through cash-flowing properties. Whether you’re purchasing your first rental or refinancing a portfolio, expert guidance makes all the difference.

Contact Stacy Ann Stephens today to discuss your options and schedule an appointment. As a seasoned Mortgage Broker at Jhenesis Mortgage, Stacy specializes in investor-friendly loans tailored to your needs.

- Stacy Ann Stephens Mortgage Broker Jhenesis Mortgage Cell: 203-910-5549 Office: 407-630-9766 NMLS#: 1933745 Email: stacyann@jhenesismortgage.com Website: https://jhenesismortgage.com

SCHEDULE APPOINTMENT now and take the first step toward financial freedom through smart real estate investing!